Retirees and the 4% Withdrawal Rule

Or, why do financial planners have such limited imagination?

More than two decades ago, Bill Bengen, a financial planner from southern California came up with a rule of thumb for how retirees should withdraw their money annually. Basically, you remove 4% (now updated to 4.5%) of your total nest egg each year. If all goes well you will have enough money for 30 years.

Critics of the rule point out that it is based on conditions in the United States during a very specific time in history; it also doesn’t take into account items like investments costs, taxes, different time horizons or the reality that most retirees don’t spend their money in a linear fashion.

I find both the rule and the underlying conservative philosophy counter-productive for today’s retirees.

First, we have to change what we mean by the word retire. If you spend time managing your money (rather than paying someone 1%) by reading about the economy, following newsletters and experts in the field, and then placing some of your money into investments you deem worthy, is that considered work?

What if you get a part-time job for 15 hours a week? I guess you're now partially retired. Consider this:

Maria Boyd-Scott turned 60 last month, and she and her wife, Joey Boyd-Scott, 68, celebrated the milestone in style: They flew business class to Amsterdam, staying at a Hilton for two nights, and then headed to France for two nights at the Waldorf Astoria Versailles.

The damage to their wallets? Thanks to their part-time travel jobs, their flights cost $462 total — they paid only the taxes. The Hilton in Amsterdam was $55 a night and the five-star hotel in France was $75 a night. The Boyd-Scotts estimate the trip could have cost upward of $6,000.

When it comes to financial planning for older people, there tends to be lots of rules of thumb, especially for those who cannot pay for personal financial advisors.

There’s the 60/40 rule:

The strategy allocates 60% to stocks and 40% to bonds — a traditional portfolio that carries a moderate level of risk.

More generally, “60/40” is a shorthand for the broader theme of investment diversification. The thinking is: When stocks (the growth engine of a portfolio) do poorly, bonds serve as a ballast since they often don’t move in tandem.

As you get older you reverse the strategy so that you have less risk with stocks and go 60% bonds and 40% stocks. There are even funds that re-balance your portfolio based on your future retirement date. For example there’s the Vanguard Target Retirement 2025 Fund, which is targeted for people retiring in 2025.

What is the Goal?

If the goal is to live on the recommended 4.5% withdrawal of your nest egg annually (plus your pension), then the best way to achieve that goal is to earn 4.5%, or close to it, for as many years as possible. In other words we want to minimize the deterioration of our assets.

Another option is to live in a country where the cost of living is low enough that your asset withdrawals are less than 4.5%.

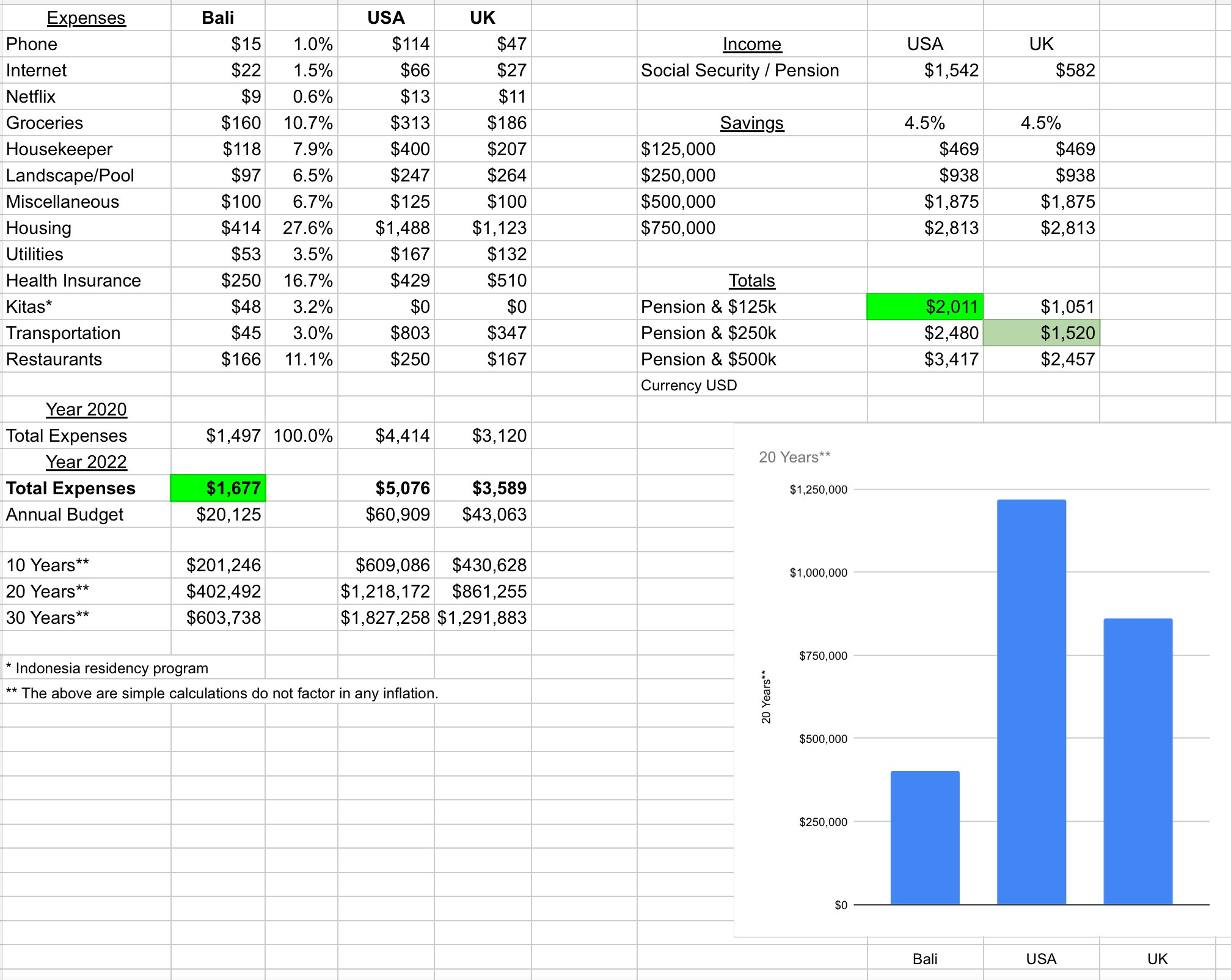

I’ve updated my original Bali cost of living spreadsheet for 2022:

For UK pension funds the average monthly payout is $582 USD (or 570 Euro). For the USA it is $1,542 USD.

If you are a UK citizen you will need a nest egg of $250,000 USD or 245,000 Euros plus your modest pension to make it work in Bali. For USA potential expats it is even easier. You can get by with $125,000 of savings and the average social security payout of $1,542.

Goal #2

Figure out a way to obtain more stable and long-lasting income. One method is to invest in real estate. There are private funds for rich folks, but now there are also Real Estate Investment Trusts via the stock market. Vanguard Real Estate ETF (NYSEARCA: VNQ) is one of the best and its expense ratio one of the lowest in the industry (.12%).

To invest more directly in an innovative and transparent company using the latest technology to disrupt the real estate sector, give Fundrise a look. They showcase each property that they buy or lease and show the results on a case by case basis.

Of course past results in no way indicates future earnings. There are several other players in this massive multi-trillion $ space.

The point of taking a quick view at an alternative investment strategy (real estate) is to show that relying on outdated rules of thumb can possibly limit one’s actions, in that for every $500,000 you only get $22,500 a year (according to the 4.5% rule of thumb). If you have less than 1/2 million $ you might think you can never retire.

These next 10 - 20 years will see amazing changes in how we live our lives. From artificial intelligence to biotechnology, every aspect of our lives is going to change, and at an accelerated pace. That means there will be new opportunities to diversify your precious nest egg.

This idea of sitting back in an easy chair and enjoying a passive retirement is not the right way to conceptualize your future. And relying on rules of thumb that are two decades old is also a bit silly.

We certainly cannot throw caution to the wind, but we can be cautiously creative. It just might mean zigging when others are zagging.

Later,

Neill

I always enjoy reading your thoughtful perspective. I have been back in Padang Linjong, Bali for a few months now living the semi-retired life managing my homes in Australia remotely. Look forward to catching up with you again for coffee.