Mental Wealth

A financial and psychological recipe

Let’s back away from retiring in Bali for a moment and discuss the mental game for obtaining financial freedom. When searching for methods to help create this new life, it seems there are two types of experts: those who focus on money and how to optimize it. And then there are those who want you to get your head in gear so that you’re in a “good place” to move forward with the life you want.

So let’s try to make a recipe that combines the two methods. First, Paula’s story:

When I graduated from college in 2005, I landed a full-time job with a $21,000 USD annual salary. Despite my low income, I decided to spend two years traveling the world. I knew that this would demand serious tradeoffs.

For the next three years, I wore clothes from thrift stores. I rode a bicycle and buses instead of owning a car. I lived in a cramped apartment. I never dyed or highlighted my hair. I didn’t have a television, home internet, or a washing machine. I slept on a free mattress I received as a hand-me-down.

In addition, I worked a "side hustle" during my evenings and weekends, writing freelance articles for 50 cents per word. I saved every penny of this side income. I got a promotion and an accompanying $10,000 USD annual raise, which brought my full-time salary to $31,000 USD per year. I saved the difference between my old salary and my new one.

It paid off. After three years, I'd managed to save $25,000 USD -- while never earning more than $31,000 USD at my full-time job.

In 2008, I quit my job, bought a one-way ticket to Egypt, and spent more than two years traveling across North Africa, Southeast Asia, Europe, Australia and New Zealand.

Many of my friends said, “I would love to do that, but I can’t afford it.”

But their hair is highlighted and their toenails are pedicured. Their clothes and furniture are new, and they’re trying the newest sushi hotspot tonight.

Please don’t misunderstand me – clothes and furniture are great things to spend money on, if that’s what you truly want.

But some people are unaware that every purchase they make is a tradeoff against something else. Every $1 you spend at a restaurant is $1 you can no longer spend traveling around the world, building a real estate portfolio or investing in your business.

The key to “affording anything” is spending money in a way that reflects your priorities.

Paula made the kind of sacrifices that are difficult for most people, but her relentless focus on prioritizing her two-year world travel plan kept her going.

Perhaps her emotional life revolved around increasing her savings each month so that her dream trip could become a reality. My sense is that a person like Paula could sustain herself emotionally as long as her saving’s account was increasing in value. That can be a potential problem, as she put all of her psychological eggs in that one travel basket.

The 4% rule:

Many financial advisors claim that you can give up working and live on 4 percent of your investment portfolio every year. For example, $750,000 USD in your portfolio means you can live on $30,000 USD each year.

I disagree with this line of thinking because it can be a roadblock for those who don’t have massive amounts of assets.

Many countries have pension systems to support elderly populations.

The Melbourne Mercer Global Pension Index is calculated using the weighted average of three sub-indices. The average sub-index scores for all 37 countries were 60.6 for adequacy, 69.7 for integrity, and 50.4 for sustainability.

Secondly, you can live off of far less than $30,000 USD a year, especially if you are willing to consider re-locating to a developing country. Or you can switch to a minimalist lifestyle. There are creative options.

Thirdly, if you do have a private or public pension plan (social security, etc) you will be receiving that money regardless of your investment prowess.

Getting started

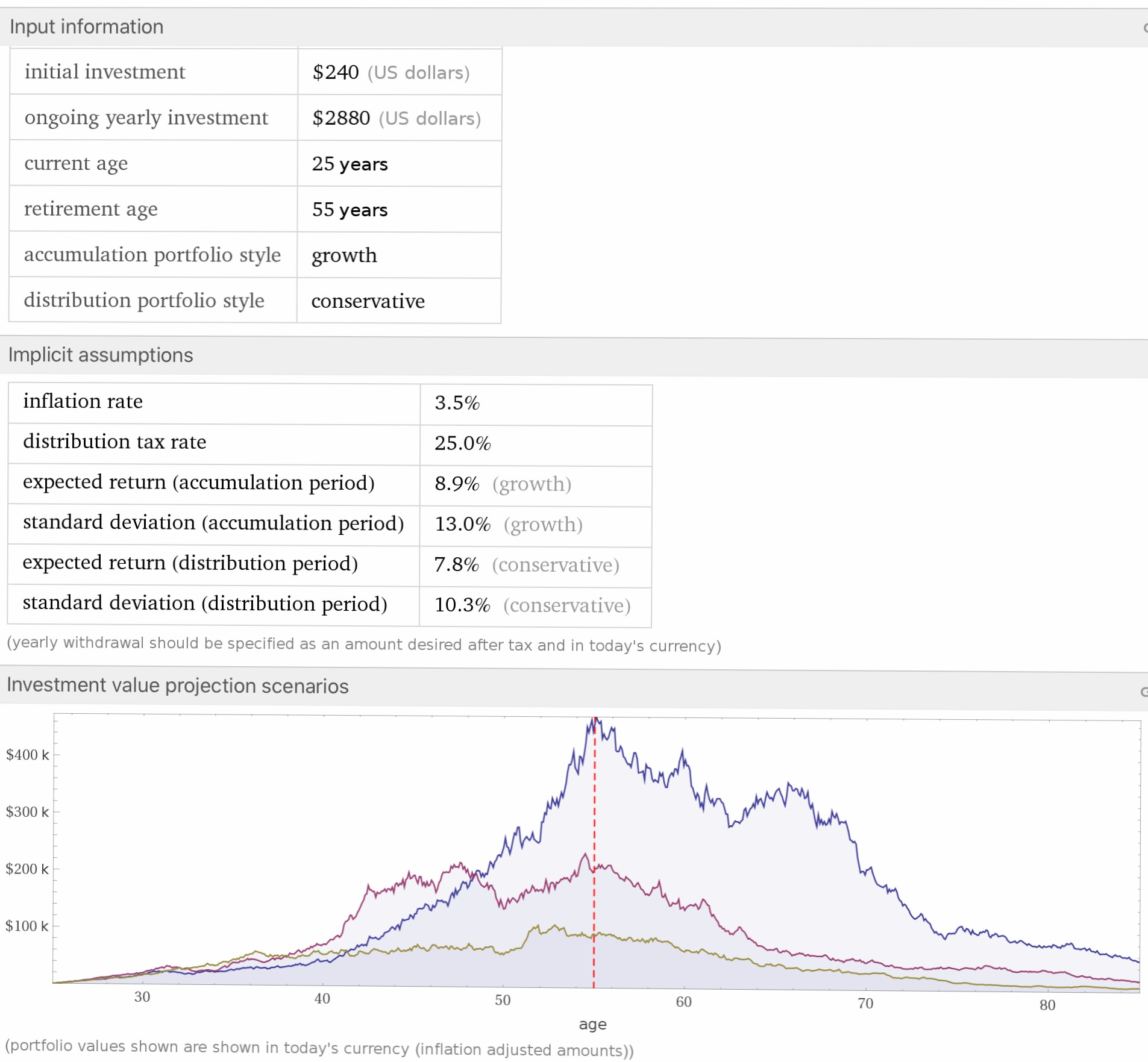

The easiest way to start is to save 1% of your salary the first month, and then increase it 1% each following month, until you reach the upper limit of your comfort zone. For example, if you earn $2,000 USD a month save $20 the first month, $40 the second month, etc. After one year you would be saving 12% of your salary or $240 USD per month.

Let’s take that $240 USD per month and invest it for 30 years:

Depending on how you invest, the returns are anywhere from $100,000 — $500,000 USD. Of course your salary wouldn’t be the same for 30 years — this is a simple snapshot.

To learn about investment options, watch this 50 minute video that offers a do-it-yourself approach:

Now let’s look at the psychological side of obtaining wealth. To be a little brash, your net worth after you’ve taken your last breath is $0, regardless of what you may leave others in terms of assets. So by that logic investing in your mind, body, and soul raises your net worth above $0. Feel rich now?

Here are the basics of maintaining mental wealth:

1. Talk about your feelings

2. Keep active

3. Eat well

4. Drink sensibly

5. Keep in touch

6. Ask for help

7. Take a break

8. Do something you’re good at

9. Accept who you are

10. Care for others

What happens when you screw up? I like this approach to how you should treat yourself:

What people often do is emphasize the negativity toward themselves. We end up saying things like:

“I’m very lazy.”

“I’m really stupid.”

“I’m extremely mean.”

“I’m totally lost.”

“I’m awfully depressed.”

The words we use to describe our negativity can be very intense. They don’t just accept a weakness, they embellish it and beat it over our heads.

We identify with the negativity in ourselves too strongly.

A better strategy is to downplay this negativity by using much less intense words. We can actively do this by saying things like this instead:

“Sometimes, I’m a little bit lazy.”

“Sometimes, I can be kind of stupid.”

“Sometimes, I’m sort of mean.

“Sometimes, I feel a little bit lost.”

“Sometimes, I’m kind of depressed.”

It’s a small change in how we talk about ourselves, but it can make a world of difference over time.

Now let’s substitute some financial reflections:

“I am a terrible saver of money.”

“I feel dumb that I fell for that marketing pitch and spent money on something I never use.”

“Learning about investing depresses me.”

“I’ll never have enough money to obtain financial freedom.”

When we use the word “sometimes” it softens the blow:

“Sometimes I do fall for a clever marketing pitch and now the product is collecting dust in my closet.”

“Sometimes I do make poor investment decisions, such as selling when the market drops, because I panic too easily.”

“Sometimes I go out to dinner with friends and we splurge on that extra bottle or two of wine.”

We are human. We fail to prioritize. We procrastinate. We choose short-term pleasures over longer term gains.

So here we go. An everyday recipe:

Save more than you spend

Invest simply* and wisely**

Don’t beat yourself up (even if financial freedom takes longer than you’d like)

*Invest in broad-based index funds (see above video). **No panic selling. Hold until you're not exactly old, just ready to begin your financial independence.

Later,

Neill

This is similar advice as found in the documentary, Warren Buffett: Bloomberg Game Changers (2012), about the billionaire investor who became the world’s wealthiest person by buying stocks from companies that were: easy to understand, well managed, competitive, enduring, and profitable businesses.

https://moviewise.wordpress.com/2014/06/27/warren-buffett/